The stablecoin float hunting for onchain yield sits near $300B, while tokenized real-world assets (RWAs) on public chains have climbed to roughly $32B in distributed value. The intersection between those two pools lies heavily in the product wrapper and surrounding ecosystem, and Maple Finance has built one of the cleaner examples of that wrapper in syrupUSDC.

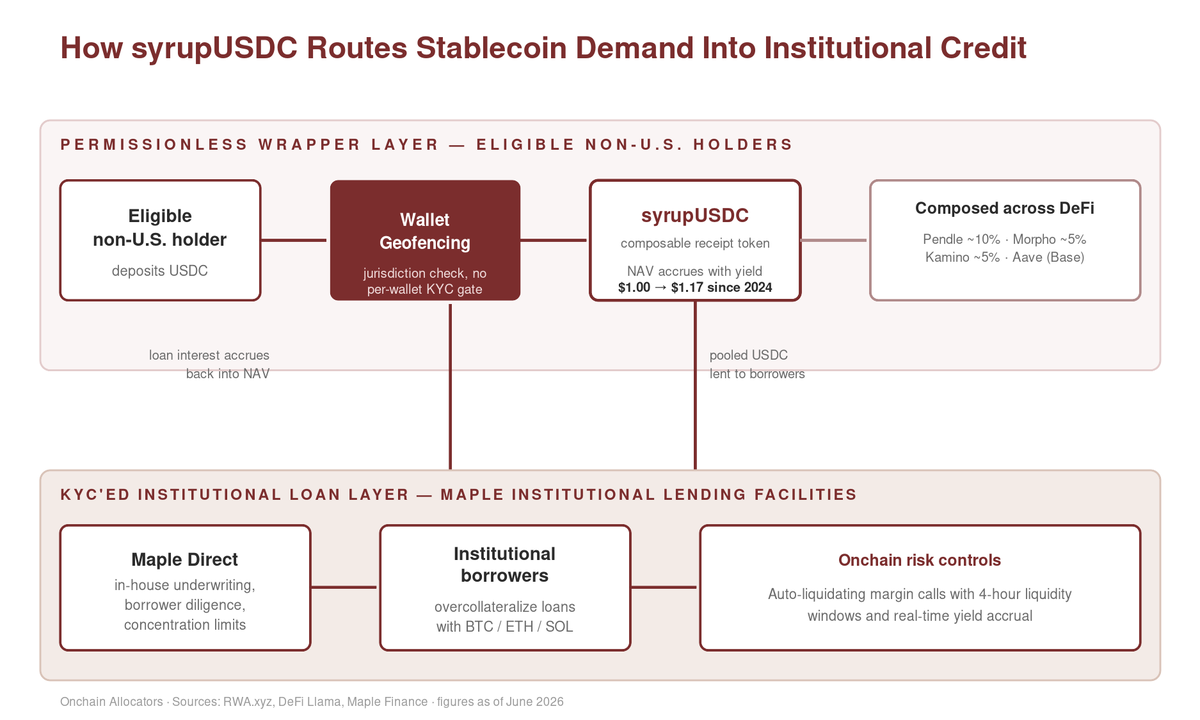

syrupUSDC takes USDC stablecoin deposited by non-U.S. holders, routes the pooled capital into overcollateralized loans to vetted institutional borrowers, and pays the interest back through a single composable token any eligible wallet can hold without clearing a per-investor compliance gate. Maple has scaled past $4.5B in assets under management (AUM) with $1.3B on the back of this syrupUSDC design, with cumulative loan originations now north of $20B.

This matters to an RWA issuer because the access model inverts how most tokenized credit reaches the market. A KYC-gated tokenized fund whitelists each wallet before it can subscribe. This is the case with Maple's flagship listings Maple Institutional - Secured Lending and Maple Institutional High Yield offerings to Reg D accredited investors and Qualified Purchasers (QPs). Tangentially to these Maple Institutional offerings is syrupUSDC, which accrues yield drips from the Institutional offerings and lets the token itself circulate among retail non-US investors. That same pattern, a permissionless yield-bearing receipt sitting on top of a gated institutional strategy, is replicable by managers willing to copy it, and the ones who do reach a distribution base a whitelist-only fund never touches. This is a model some RWA issuers have begun recreating in other asset classes (reinsurance, CLOs), but Maple's first-mover advantage and tailored crypto lending niche continue to propel it across the industry.

How a Permissionless Token Carries Institutional Loan Yield

The elegance is in what the syrupUSDC holder does not have to do. An eligible non-US depositor sends USDC to the Syrup pool and receives syrupUSDC, an accumulating token whose net asset value (NAV) appreciates over time with retained yield distributions rather than paying a separate coupon to tokenholders. Underneath, Maple lends that pooled capital to institutional borrowers who post crypto collateral worth more than the loan and pay interest on it. syrupUSDC was recently trading near $1.17 against its original $1.00 mint in May 2024, the price reflecting an increased cumulative NAV due to the underlying retained yields from the lending pools syrupUSDC accesses.

At the time of writing, syrupUSDC yields 4.80%, roughly 40bps over the 10-year US Treasury rate and almost 10bps over the 3-month US Treasury rate. This is an interesting profile because while Maple's loans are overcollateralized, they're all purely crypto. Nonetheless, Maple garners assets from DeFi and crypto-natives plus institutions like Cantor Fitzgerald alike.

Risk management and collateral monitoring happens one layer above syrupUSDC at the individual lending facilities. Borrowers, which typically include hedge funds, investment firms, market makers, and crypto exchanges, 1) stay overcollateralized in BTC, ETH, or SOL held in Maple's custody contracts, 2) are automatically margin called within 24 hours as collateral approaches liquidation, and 3) sit under concentration limits that cap any single exposure. Margin calls have been met on average within four hours, and the secured book recorded zero losses through the October 10, 2025 liquidation cascade across the industry. Think of syrupUSDC as the institutional loan book repackaged into a building block that settles, composes, and moves at the speed of a smart contract throughout DeFi. It brings mutual tremendous value as a collateral asset to lending protocols and yield investors, which has fed its growth flywheel very well.

Where the Yield Stacks Up in the Industry

An allocator does not underwrite a 4.70% net rate in isolation, and the spread only matters against the products competing for the same dollar. Aave's USDC supply market clears near 3.34%, BlackRock's BUIDL tokenized Treasury fund runs roughly 3.50% to 4%, and Franklin Templeton's BENJI money market token carries a trailing yield near 3.86%. Ethena's sUSDe, the synthetic-dollar savings token, has compressed into the high-3% range as perpetual funding cooled from its 2024-2025 stretch that swung anywhere from 4% to 30%. This is likely the right cohort for syrupUSDC given the short duration and near-immediate liquidity avenues of each. Against that set, syrupUSDC's base sits at the top of the money market cohort while sourcing its yield from a different engine entirely: overcollateralized loans.

Regulatory and Compliance Setup

The access model is key for all allocators to understand and get comfortable with. Maple offers a range of individual direct lending facilities for US accredited investors via Reg D exemptions. It also, of course, offers syrupUSDC as a blanket-coverage token to underlying facilities for non-US retail investors. Eligibility for syrupUSDC runs through geofencing that excludes US persons and restricted jurisdictions.

Said differently, syrupUSDC's compliance setup is jurisdiction-based rather than individual investor-based. This is different than the KYC gated subscription model behind the AAA collateralized loan obligation (CLO) funds covered in a prior edition, where each allocator onboards KYC/AML and gets a single wallet whitelisted before subscribing.

The syrupUSDC Advantage in DeFi

The permissionless wrapper of syrupUSDC effectively reaches the entire non-U.S. stablecoin-holding population plus every protocol that integrates the token as collateral. Maple has been on a roll with protocol integrations like Morpho, Kamino, and Byzanlink now supporting syrupUSDC as collateral. The collateral can be looped and leveraged, with investors banking on Maple Finance's overcollateralization practices and underwriting to preserve principal value in syrupUSDC. This creates a superior collateral asset to holding and leveraging a raw cryptocurrency.

Overcollateralized crypto lending collateral is originated onchain and self-liquidating, so the wrapper carries no off-chain enforcement burden. It extends cleanly to other crypto-collateralized credit and to permissionless secondary money market wrappers in the spirit of the Ondo USDY and Backed precedents, where the underlying is a liquid, transferable instrument. It does not necessarily extend easily to traditional lock-up funds and private credit BDCs that require manual transfers and longer-term liquidity / redemption periods. Knowing which RWA classes can wear this wrapper and which cannot is a difference maker.

What makes the wrapper sticky once it travels is the integration flywheel, and Maple's deployment data backs that up. Of syrupUSDC's $1.3B in supply, roughly 10% sits in Pendle, near 5% in Morpho, and near 5% in Kamino on Solana, while close to all of the Base supply is deployed on Aave. Each integration increases the stickiness of the token and makes the wrapper harder to displace, because unwinding it means unwinding every venue that now accepts it as collateral. That accumulating lock-in is the goal for DeFi-focused issuers.

A Standing Bid, and the Risk of the Composability Itself

A key takeaway from this breakdown is that onchain capital, and now the fintechs distributing onchain assets to mainstream users, likely prefer a composable yield token over numerous bespoke facilities wherever plausible, and that creates a standing bid for permissionless wrappers built on institutional-caliber underwriting like in Maple's case.

Maple initiated its syrupUSDC token as a mechanism to bring its platform yields to the general masses. Everything remains fully compliant on the individual loan facility levels, with access granted only to successfully KYC'ed accredited and institutional lenders. Given the success and the desire for DeFi composability, the industry may likely see 10+ RWAs with similar 'syrupUSDC-like' structures across CLOs, Private Credit, Trade Finance, and other underwriteable assets with manageable liquidity profiles.

— Peter Gaffney, Head of DeFi

This article is for informational purposes only and does not constitute investment advice. Eligibility for products like syrupUSDC is restricted and jurisdiction-dependent, so verify your own status before acting.