Tokenized real-world assets (RWAs) are meeting onchain demand for predictable dollar yield. RWAs on public chains crossed nearly $24B in March 2026, up roughly 66% since the start of the year, while the stablecoin float that hunts for onchain yield remains solidly at $300B.

Pendle Finance, the onchain interest-rate market that splits any yield-bearing asset into a Principal Token (PT) that redeems at par on a fixed date and a Yield Token (YT) that captures the variable return through maturity, is one of the industry's OGs in composable yield. Pendle has quietly become an RWA layer on which tokenized yield assets turn into something an institutional allocator can actually underwrite. This upgrade stems from its PT/YT structure converting variable tokenized fund yield into fixed-rate income strips, enabling the tranching and junior-senior structures allocators are accustomed to.

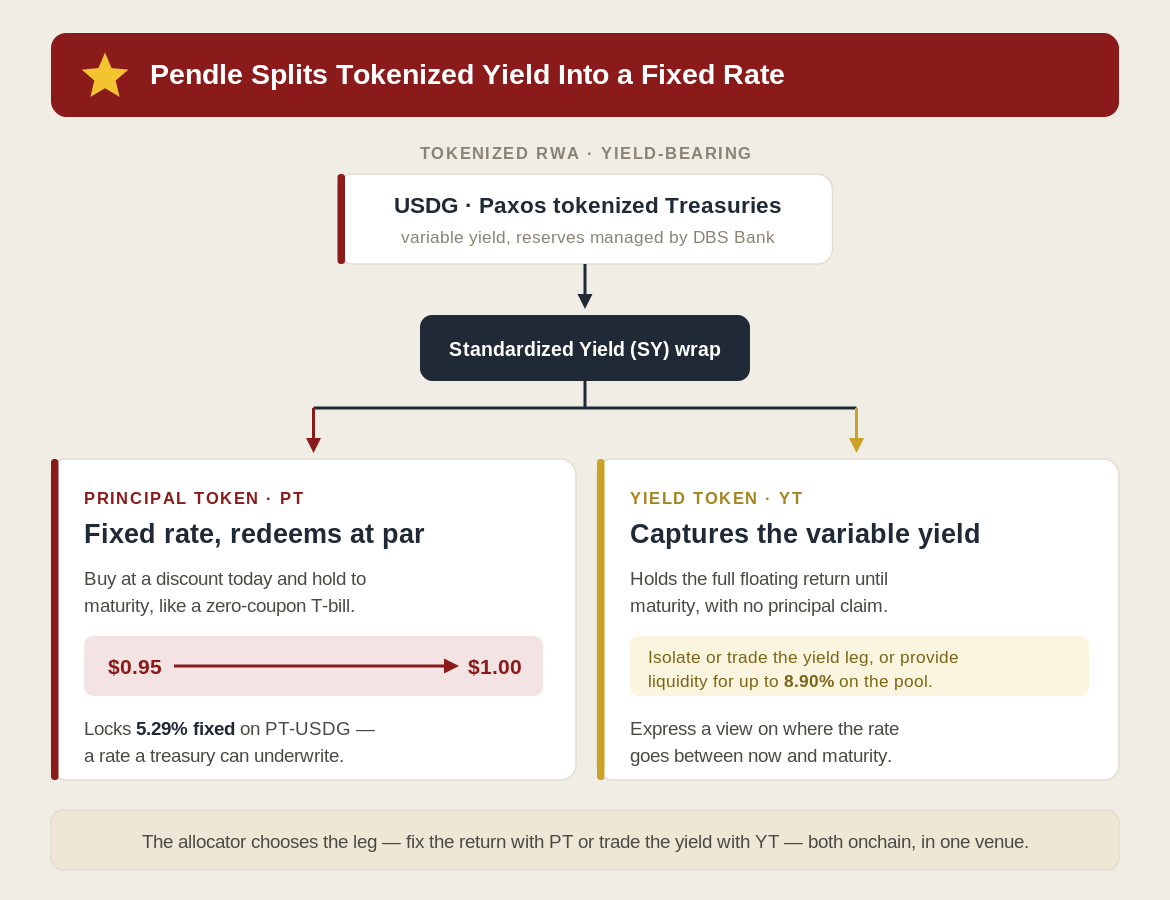

Pendle Converts Variable Tokenized Yield Into a Fixed Rate

The reason this matters to a treasury is that most tokenized RWA products pay a floating rate, and a floating rate is difficult to budget against. There are numerous fixed-term platforms coming to market like Loopscale, Tenor Finance, and Morpho's fixed-term markets as the industry demands less reliance on overcollateralized borrowing and floating-rate "DeFi Money Markets." Pendle addresses this by letting an allocator buy the Principal Token at a discount and hold it to maturity, which behaves like a zero-coupon bond that moves from say $0.95 to $1.00 at a known date, locking a fixed return regardless of what the underlying yield does in the interim.

The clearest RWA example with Pendle is Paxos's USD Global Dollar (USDG), a regulated, Treasury-backed stablecoin whose reserves are managed by DBS Bank and overseen by the Monetary Authority of Singapore (MAS), and compliant with the European Union's MiCA framework. When USDG debuted on Pendle it cleared nearly $46M in Total Value Locked (TVL) within weeks, offering a fixed 5.29% on PT-USDG and up to 8.90% for interested liquidity providers. For an institutional treasury exploring onchain fixed income for the first time, that is the risk-free TradFi rate wrapped in a form a smart contract can settle, with no brokerage and no off-chain custodian in the path. The setup opens a very powerful door to DeFi-native borrowing, margining, and swapping — all technically backed by a real-world asset.

Looping Is the Leverage Engine Underneath

Fixed-rate exposure is the entry point and leverage on it is where onchain allocators start moving real size. Reference the Apollo Diversified Credit Securitize Fund (ACRED), a tokenized feeder into Apollo's $1B diversified credit strategy that has been live since January 2025. Securitize and Gauntlet, one of the industry's leading vault curators, built a levered RWA strategy on Morpho where the workflow runs as the following loop: 1) an allocator deposits ACRED, 2) borrows USDC against it, 3) buys more ACRED, and 4) repeats until target LTV. Gauntlet's risk engine manages the leverage ratio so the position does not unwind in predetermined drawdown scenarios. Obviously looping and leveraging assets recursively in this manner adds risk beyond the standalone RWA; this is nothing new in DeFi.

That same credit yield now reaches Pendle's PT/YT markets through an ERC-4626 access point, which means an allocator can take the floating credit return and either fix it for the duration of the term or isolate the variable yield leg entirely. Think of it as the difference between owning a credit fund and owning a tunable instrument built on top of one, where the duration, the leverage, and the fixed vs. floating rate decision are all actionable onchain in a single venue.

DeFi Delivery Is the Product, and the Yield Is the Commodity Underneath

The lesson from this category is the same one that has been playing out in tokenized credit since late 2024, which is that tokenizing the fund is table stakes and building the ecosystem that lets onchain allocators use it is where the value accrues. A TradFi manager that mints a token and lists it has done the easy part; a manager whose product flows into Pendle as a PT, into Morpho as collateral, and into a looped strategy with a capable risk curator has built the surrounding ecosystem that actually draws in onchain capital. The data shows where that delivery is landing, as Pendle has settled nearly $70B in cumulative fixed yield and runs north of $5B in TVL across 11 networks, with the RWA slice of that book climbing toward $150M over roughly eight months as tokenized Treasuries, corporate credit, and private credit migrate in. Stickiness matters here, as every protocol that wires a wrapped ACRED or PT-USDG in as collateral raises the switching cost of choosing a newer venue, producing the same integration lock-in and TVL flywheel that rewards the issuing manager with additional assets under management (AUM) and fee capture.

Composability Accelerates Onchain Fixed Income

The signal in Pendle's RWA build-out isn't merely that allocators like fixed rates. That notion has existed since the dawn of capital markets. The real signal is that onchain capital will choose a tokenized fund that arrives with a full delivery stack — fixed-rate composability, collateral utility, and a looping path — over an equivalent that exists simply as a bare token. This creates a major mismatch in supply-demand dynamics resulting in the same handful of RWAs gathering the majority of capital inflows. The ability to tranche and compose yields with Pendle and similar services should expand this palette and create more supply-side competition for allocators to feasibly evaluate.

— Peter Gaffney, Head of DeFi

This article is for informational purposes only and does not constitute investment advice. Eligibility for products like USDG or ACRED is restricted and jurisdiction-dependent, so verify your own status before acting.